- InvestorThread

- Posts

- Use 'Iron Condor' to Place Parlay Bet on Novo Nordisk

Use 'Iron Condor' to Place Parlay Bet on Novo Nordisk

There’s up to 88% yield in NVO stock available for dice rollers

InvestorThread

October 29, 2024

By Josh Enomoto

I’m going to be blunt: I don’t know a whole lot about Novo Nordisk (NYSE:NVO) other than the obvious. As a Danish multinational pharmaceutical company with a great pipeline, its market capitalization of over $382 billion makes it one of the underlying ecosystem’s powerhouse enterprises. But at the end of the day, mere knowledge of key financial metrics will not reliably predict where NVO stock will head next.

Still, as a major player in the pharmaceutical space, the equity probably isn’t going to bounce wildly. Sure, the company has an earnings report coming up (slated for Nov. 6). However, NVO stock is a known commodity. After going on a blistering run earlier this year, investors have clearly decided to take profits. In the past six months, shares have slipped more than 11%.

However, the volatility may eventually fade as both bulls and bears have had their fair share at the Novo Nordisk buffet. Technically, this is hardly an unreasonable assumption. Presently, the company’s 60-month beta sits at 0.42, well below the benchmark equity index’s beta of 1.0. Basically, NVO stock is significantly less volatile than the broader market.

Should NVO stock trade within a defined price range, it would be difficult to profit from a directional trade. However, investors can use an options strategy called the iron condor to effectively place a parlay wager on the Danish company’s shares.

On the Hunt for Wild Condors

For those who are anticipating a reduction in implied volatility (IV) in the target security, an appropriate strategy may be the short iron condor. The term short refers to the position starting from a cash inflow state; that is, we would have a net short position to generate income off the sale of options.

Specifically, the short iron condor is a combination of the bear put spread and bear call spread. By logical deduction, this particular condor features four legs: one pair representing the profitability zone of the lower boundary (bear put) and one pair representing the profitability zone of the upper boundary (bear call).

As you might surmise, the goal is to have the stock stay inside the range of the inner strike prices.

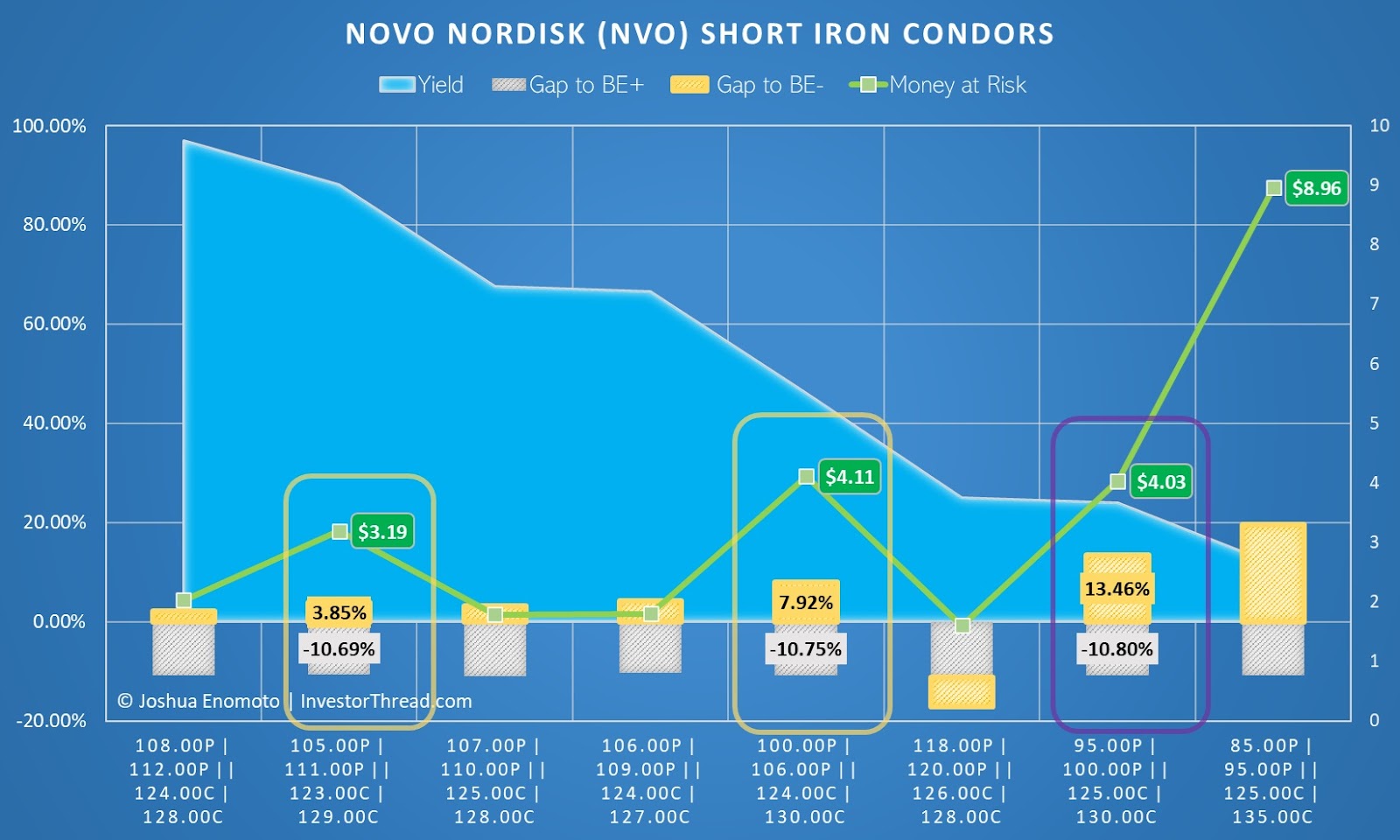

Initially, short iron condors may appear intimidating. For example, the options chain expiring Nov. 15 features 185 different condor candidates, according to Barchart. That’s a lot of data to sift through but I’ll let you in on a little secret: you really don’t have to deal with all that crap.

In a list of hundreds of condors, only a handful of prospects are actually worth your time.

First and foremost, we must establish a baseline trade. This is the condor that offers the highest yield that mathematically meet the minimum criteria for projected success. In other words, the “wings” of the condor can cover the expected up/down price swings of the target security.

But how do we calculate this expected kinesis? We apply a stochastic calculation where we multiply the below metrics:

Current share price

The average IV of the target options chain (expiration date).

Time decay adjustment (the square root of the number of calendar days to expiration divided by 365 days).

For NVO stock options expiring Nov. 15, the product of the above three metrics clocks in at nearly $12.73. Therefore, the upper breakeven price for our baseline condor must be at least $125.09 or higher and the lower breakeven price must be $99.63 or lower.

Looking at the data, the trade that meets these price thresholds while still yielding 24.07% is the 95.00P | 100.00P || 125.00C | 130.00C condor. Here, the upper breakeven is $125.97 and the lower breakeven is $99.03.

Modifying Our Wager on NVO Stock

Still, our baseline iron condor leaves much to be desired. For one thing, the yield is merely okay at 24%. Unfortunately, we would have to put up $403 at risk to earn $97. All it takes is for this bet to go bad to put a damper on our other bets.

Let’s assume that you don’t anticipate NVO stock rising above $125 but not falling below $100. You could trim some of the lower boundary safety margin and go with the 100.00P | 106.00P || 124.00C | 130.00C condor. This trade lowers your upper breakeven to $125.89 and raises your lower breakeven to $104.11. In exchange, the yield jumps to just under 46% and the amount of money at risk is almost unchanged at $411.

For an even more aggressive bet, you can consider the 105.00P | 111.00P || 123.00C | 129.00C condor. This will narrow your upper and lower breakeven prices to $125.81 and $108.19, respectively. But as a potential reward for the higher risk profile, you would get a yield of 88.09%.

And that’s about it. If you try to squeeze your margins further, your lower breakeven price would rise to the $110 level. Considering that NVO stock is just below $112 in Tuesday’s premarket activity, that’s arguably a risk not worth entertaining.

Disclaimer: The author did not hold a position in any of the securities mentioned above. The information provided in this article is for educational and informational purposes only and should not be construed as investment advice. Always conduct your own research or consult with a licensed financial professional before making any investment decisions. Past performance is not indicative of future results.