- InvestorThread

- Posts

- Spirit Airlines (SAVE) Offers a One-Week Ticket to a 72% Yield

Spirit Airlines (SAVE) Offers a One-Week Ticket to a 72% Yield

A short iron condor beckons the extreme speculator

InvestorThread

October 25, 2024

By Josh Enomoto

Author and financial expert Harry Dent once compared the ebb and flow of market dynamics to the male orgasm. It’s an interesting parallel, in large part because he’s probably right. Following an outpouring of euphoria, the tango usually ceases due to exhaustion. Not unlike the situation with Spirit Airlines (NYSE:SAVE).

I’m not going to spend too much time reinventing the wheel here. Following a worrying erosion in SAVE stock since a federal judge placed a roadblock on efforts by JetBlue Airways (NASDAQ:JBLU) to buy out its rival low-cost carrier, Spirit managed to stave off immediate bankruptcy concerns with a debt refinancing agreement.

In addition, The Wall Street Journal is reporting that the embattled carrier and Frontier Airlines (NASDAQ:ULCC) are in talks regarding a possible merger. Should positive news officially materialize on this front, SAVE stock could skyrocket. On the other hand, if the fairy tale ends poorly, long-term stakeholders could suffer even more damage.

Put another way, Spirit could see its implied volatility (IV) — or the market’s expectation of the magnitude of forward movement — swing even higher from its already-elevated perch. Near the close of the midweek session, SAVE’s IV reached 245.59%, a simply stunning figure.

Nevertheless, in the near term, it’s more than possible that implied volatility could decelerate. SAVE stock gained almost 46% on Wednesday. Speculators will likely take some profits and in the absence of fresh news, shares could enter a temporary consolidation range.

Short Iron Condor Tempts Gamblers of SAVE Stock

Given the blistering run in SAVE stock, the natural temptation focuses on going in the opposite direction. Certainly, shorting the security has its case. Just a few days ago, the equity was poised to drop to the $1 per share level. Yes, some deals and rumors have materialized but did they really change the core of the argument?

I think most people would wager not.

Nevertheless, a directional bet might not appeal to every speculator. For a more nuanced approach, one could consider — if they’re willing to take extreme longshot odds in the first place — the short iron condor. This multi-leg options trade (which starts from a cash inflow position, hence the term “short”) assumes a transition from high IV to low.

Effectively, it’s a combination of a bull put spread and a bear call spread. Structurally, the trader makes money when the security in question rises above the bull put’s credit leg but below the bear call’s equivalent. In other words, the stock must stay within a defined range: not too high, not too low.

As expected, the short iron condor’s pricing mechanism is as follows: the higher the risk, the higher the reward (or yield, since we’re talking about a credit-based approach). However, options market pricing is nowhere near as efficient as that found in the open market. Therefore, it’s possible to find what is mathematically the most efficient trade based on a particular directive.

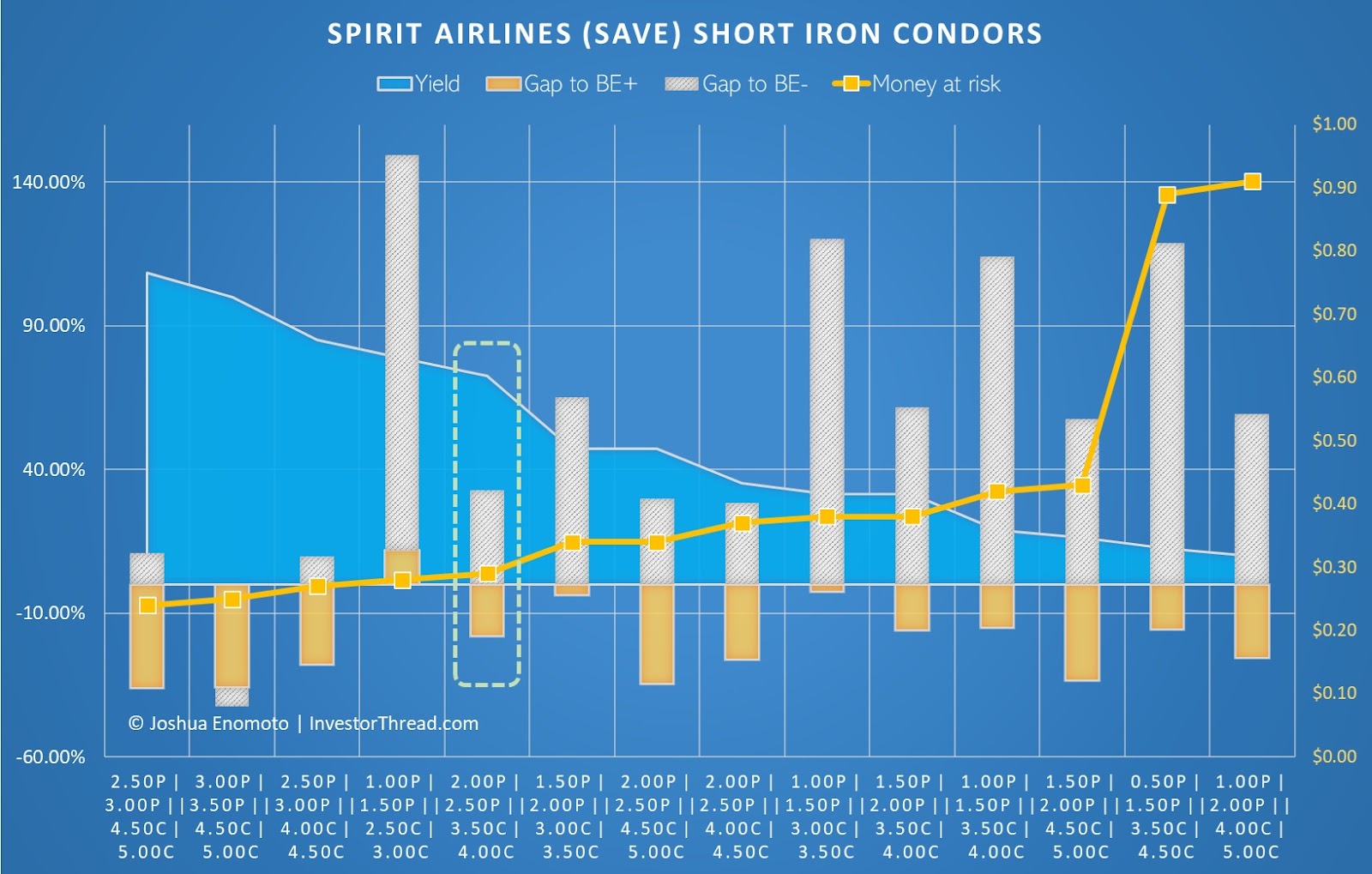

I won’t leave you in suspense: the iron condor for the options chain expiring next Friday (Nov. 1) that I’ve calculated offers the most ideal balance between risk and reward is the $2.00P(ut) | $2.50P || $3.50C(all) | $4.00C.

With a maximum possible yield of 72.41%, the reward is arguably adequate for the $29 at risk for the trade. Further, based on a SAVE stock share price of $3.04, the gap to the upper breakeven (BE) profitability threshold ($3.71) clocks in at 18.06%. The gap to the lower BE ($2.29) lands at 32.75%.

On an absolute basis (adding the percentage width to the upper and lower BE boundaries), you’re looking at 50.81%. That’s a lot of margin for SAVE stock to move around until the trade becomes unprofitable.

Not a Big Fan of the Other Condors

With the chart I provided, you can quickly see why I’m not a big fan of the other condors available. For instance, with the $1.50P | $2.00P || $3.00C | $3.50C, the BE “width” in absolute terms stands at 69.01%. However, most of this cushion is geared toward the lower BE threshold. There’s not much room to the upside for this condor.

Plus, this trade suffers from a severe drop in yield to 47.06%. If you want more margin (i.e. width to the BE thresholds), you will incur additional yield penalties. By logical deduction, the reduced yield also means that you’re putting more money at risk. With the first condor, you enjoy a more balanced profile with a healthy reward should the trade go smoothly.

Of course, I’m not guaranteeing anything here. The short iron condor has many moving parts so it’s very risky. At the same time, there is a science to picking the right idea. If you’re going to roll the dice, you should do so in the most efficient manner possible.

Disclaimer: The author did not hold a position in any of the securities mentioned above. The information provided in this article is for educational and informational purposes only and should not be construed as investment advice. Always conduct your own research or consult with a licensed financial professional before making any investment decisions. Past performance is not indicative of future results.